Interest Rates: Hungarian central bank (NBH) Governor Zsigmond Járai is quoted on Wednesday as saying that "It was a bad decision...A 25 basis point hike would have signaled that we are defending the inflation goal".

The problem is, what do you do when there are very few good decisions available. Raising rates holds inflation, but raises the forint (which makes exporting difficult) and raises the cost of government borrowing (incidentally there are a hell of a lot of short term bonds changing hands at the moment).

Meantime Járai reasserts his commitment to price stability:

Hungary's central bank (NBH) has not given up its aim of price stability as it is trying to prevent that an economic slowdown comes with rising inflation, Governor Zsigmond Járai said on Wednesday.

"The following period will be an era of uncertainties with toned down growth and inflation risks. The objective of the central bank is to avoid staglflation and so it does not give up its endeavours to reach price stability, Járai told a conference.

The NBH's Monetary Council decided to keep the base rate on hold at 8.00% on Monday, after five successive monthly rate hikes of 200 basis points in total, but Járai said that an interest rate hike was still on the cards.

"If we see that the inflation target is in danger, the NBH will tighten monetary policy," Járai said.

The bank in its quarterly inflation report cut its forecast for 2008 average annual inflation to 4.1% from 4.2%, above its medium-term target for 3%, confusing some analysts who had expected a rate hike.

At the same time, the NBH slashed its core inflation forecast for 2008 to 4.0% from 4.4%.

Monday, November 27, 2006

Thursday, November 23, 2006

Flextronics Reduce Staff

Obviously it is impossible for me to comment on individual cases, and the reasons why Flextronics lost their order with the 'important client' which means that 30% of the 2,000 odd workforce will now be laid off. I would simply say that if you look at the comparatively high value of the forint, and take into account the rather high rate of inflation, then this type of problem is only to be expected.

Flextronics International Ltd., the world's largest manufacturer of custom-made electronics, is firing about 30% of staff at one of its four Hungarian plants after losing a major client.

About 2,000 permanent and temporary employees currently work at the factory in Nyiregyháza, northeast Hungary, Péter Papp, the director of human resources for eastern Europe, said in a telephone interview today. “We have hired more than 1,000 workers in the past six months at the plant and with this major client taking away production we need to cut jobs,” Papp said. “The dismissal of 590 by early February is the worst-case scenario because we'll try to help them find jobs within the company.” Flextronics also has plants in Tab, southwest Hungary, Zalaegerszeg in the west and Sárvár in the northwest. The company will employ just under 10,000 after the Nyiregyháza dismissals, Papp said, adding the company will remain one of the Hungary's 10 largest employers. Papp declined to identify the client that canceled its contract or say which product Flextronics made for it, except that it was sold in large volumes around Christmas. Napi Gazdaság reported the job cuts news earlier today.

Flextronics International Ltd., the world's largest manufacturer of custom-made electronics, is firing about 30% of staff at one of its four Hungarian plants after losing a major client.

About 2,000 permanent and temporary employees currently work at the factory in Nyiregyháza, northeast Hungary, Péter Papp, the director of human resources for eastern Europe, said in a telephone interview today. “We have hired more than 1,000 workers in the past six months at the plant and with this major client taking away production we need to cut jobs,” Papp said. “The dismissal of 590 by early February is the worst-case scenario because we'll try to help them find jobs within the company.” Flextronics also has plants in Tab, southwest Hungary, Zalaegerszeg in the west and Sárvár in the northwest. The company will employ just under 10,000 after the Nyiregyháza dismissals, Papp said, adding the company will remain one of the Hungary's 10 largest employers. Papp declined to identify the client that canceled its contract or say which product Flextronics made for it, except that it was sold in large volumes around Christmas. Napi Gazdaság reported the job cuts news earlier today.

Lajos Bokros the Hungarian Cavallo?

Domingo Cavallo is perhaps best known to economic history as the financial supremo who leaped to the headlines during his term as Argentina's Economy Minister in 2001 as he battled with the looming economic crisis which finally burst in January 2002. (Not everyone of course shares this view and an alternative point of view on Domingo Cavallo can be found here).As Robert Barro noted:

In March, 2001, President Fernando de la Rúa's new Economy Minister, Ricardo López Murphy, failed when a reasonable program of curtailing public spending hit a political roadblock. Now there is talk in the markets of default on Argentina's foreign debt.

Out of desperation, the President has turned to his political rival, Cavallo, to save the economy a second time.

Now it seems Lajos Bokros is offering himself for a somewhat similar role in the context of Hungary's growing economic crisis. Of course, the parallels do not end there, since Cavallo was also the architect of Argentina's economic reform process during his tenure at the Ministry in 1991:

Things changed in 1991, when Domingo Cavallo took over as Economy Minister. His reforms were pro-market and featured fixing the peso at 1-to-1 parity with the U.S. dollar. He also pushed trade liberalization and reforms of public finance and the banking system. Despite the recession of 1995, induced by the Mexican peso crisis, Argentine per capita GDP grew at an average rate of 4.8% during the Cavallo years, through 1996.

And of course Lajos Bokros - currently Chief Operating Officer and professor of the Central European University (CEU) - was Finance Minister and father of an aggressive austerity package back in 1995:

Lajos Bokros, Hungary's former Finance Minister and the father of an aggressive but inevitable austerity package in 1995, said he would assume the position of Prime Minister if he was allowed to execute his own adjustment programme.

Bokros, who is currently Chief Operating Officer and professor of the Central European University (CEU), also said the country is in a political and moral crisis in respect of the fact that the governments which had been overspending and pushed the country into indebtedness can hardly ask for sacrifices from the people.

In an interview with weekly Heti Válasz, the former World Bank Director reiterated that Hungary needed a multi-insurance model in healthcare a market-based higher education and sweeping reforms in the pension regime.

With regards to the pension system Bokros said it could not be allow leaving one third of the population wrapped in cotton and let the working people carry all burden. The current system even encourages people to withdraw from the labour market via early or disability retirement, he added.

With respect to the tax cut plans of main opposition party Fidesz, Bokros said taxes would need to be reduced but that it could not be done without holding back spending more than presently.

At a conference of the central bank (NBH) Bokros said on Wednesday that what is currently hanging over Hungary is not the threat of bankruptcy or a financial crisis but the shadow of falling behind.

Growth is hampered by Hungary's huge twin deficit and the fiscal adjustment package will make Hungary the slowest growing emerging market next year, he added.

Bokros stressed the importance of structural reforms and pointed out the quality and availability of public services have been eroding, which undermines social solidarity.

Now the parallels with Argentina's situation in 2001 do not end here. Both countries share the problem of finding themselves on an unsustainable economic path, and in need of urgent measures which go beyond what the incumbernts are (or were) offering.

In Hungary's case Bokros is right to draw attention to the fact that tax increases will only add to Hungary's problems in terms of attaining the growth which is needed to support public services. He is also right that Hungary's health and pensions systems are at the heart of the problem.

But here the situations differ. Argentina had a currency peg, while Hungary's forint is, at least in theory, free floating. However since Hungary badly needs to retain foreign investment, and also needs to keep inflation in check, there is little alternative to relatively high interest rates, but these precisely (at least for the time being) maintain the forint at a relatively high level, which of course produces the same problem in exporting which Argentina suffered. These high interest rates also make the cost of servicing the government debt rather high, and this fact alone, as we have seen here, contributes to the difficulties in reducing the deficit.

The other big difference between Hungary and Argentina is the demographic one. Argentina was a comparatively high fertility developing economy, with, by and large, the phenomenon known as the demographic dividend out there in front of it. Hungary unfortunately belongs to that group of countries who went through a large part of their demographic transition before they became economically rich. As such the future lying out in front of Hungary is inevitably a complicated one, with or without the present economic conundrum. Fertility is at the lowest-low level (or see the file linked to here) and Hungary is set to age rapidly as the currently low life expectancy rises and rises. So the demographic changes which are facing Hungary involve more of a demographic penalty than a demographic dividend.

And Bokros is right to draw attention to the social spending dilemma which Hungary faces. He is also right that the pension and health systems badly need reform. The question is, as people enter a necessary private pillar, where does the money come from to finance the earlier PAYGO system, and how do you prevent the quality and availability of public services from eroding (which Bokros says he wants to do) if what you are going to do is reduce spending on them significantly? Somehow the numbers here just don't add up.

At the end of the day all comparisons are rather limited in their value. But what worries me most here is that I just can't see a sustainable path for Hungary to take hold of, and that, believe me, is the most worrying thing of all. Simply telling people that what they need is an austerity package if you have no clear idea of how the hell it can all work is only likely to mean that you end up as Cavallo did, only as I said Hungary isn't Argentina, and the end product of all this prevarication won't be a pretty sight.

In March, 2001, President Fernando de la Rúa's new Economy Minister, Ricardo López Murphy, failed when a reasonable program of curtailing public spending hit a political roadblock. Now there is talk in the markets of default on Argentina's foreign debt.

Out of desperation, the President has turned to his political rival, Cavallo, to save the economy a second time.

Now it seems Lajos Bokros is offering himself for a somewhat similar role in the context of Hungary's growing economic crisis. Of course, the parallels do not end there, since Cavallo was also the architect of Argentina's economic reform process during his tenure at the Ministry in 1991:

Things changed in 1991, when Domingo Cavallo took over as Economy Minister. His reforms were pro-market and featured fixing the peso at 1-to-1 parity with the U.S. dollar. He also pushed trade liberalization and reforms of public finance and the banking system. Despite the recession of 1995, induced by the Mexican peso crisis, Argentine per capita GDP grew at an average rate of 4.8% during the Cavallo years, through 1996.

And of course Lajos Bokros - currently Chief Operating Officer and professor of the Central European University (CEU) - was Finance Minister and father of an aggressive austerity package back in 1995:

Lajos Bokros, Hungary's former Finance Minister and the father of an aggressive but inevitable austerity package in 1995, said he would assume the position of Prime Minister if he was allowed to execute his own adjustment programme.

Bokros, who is currently Chief Operating Officer and professor of the Central European University (CEU), also said the country is in a political and moral crisis in respect of the fact that the governments which had been overspending and pushed the country into indebtedness can hardly ask for sacrifices from the people.

In an interview with weekly Heti Válasz, the former World Bank Director reiterated that Hungary needed a multi-insurance model in healthcare a market-based higher education and sweeping reforms in the pension regime.

With regards to the pension system Bokros said it could not be allow leaving one third of the population wrapped in cotton and let the working people carry all burden. The current system even encourages people to withdraw from the labour market via early or disability retirement, he added.

With respect to the tax cut plans of main opposition party Fidesz, Bokros said taxes would need to be reduced but that it could not be done without holding back spending more than presently.

At a conference of the central bank (NBH) Bokros said on Wednesday that what is currently hanging over Hungary is not the threat of bankruptcy or a financial crisis but the shadow of falling behind.

Growth is hampered by Hungary's huge twin deficit and the fiscal adjustment package will make Hungary the slowest growing emerging market next year, he added.

Bokros stressed the importance of structural reforms and pointed out the quality and availability of public services have been eroding, which undermines social solidarity.

Now the parallels with Argentina's situation in 2001 do not end here. Both countries share the problem of finding themselves on an unsustainable economic path, and in need of urgent measures which go beyond what the incumbernts are (or were) offering.

In Hungary's case Bokros is right to draw attention to the fact that tax increases will only add to Hungary's problems in terms of attaining the growth which is needed to support public services. He is also right that Hungary's health and pensions systems are at the heart of the problem.

But here the situations differ. Argentina had a currency peg, while Hungary's forint is, at least in theory, free floating. However since Hungary badly needs to retain foreign investment, and also needs to keep inflation in check, there is little alternative to relatively high interest rates, but these precisely (at least for the time being) maintain the forint at a relatively high level, which of course produces the same problem in exporting which Argentina suffered. These high interest rates also make the cost of servicing the government debt rather high, and this fact alone, as we have seen here, contributes to the difficulties in reducing the deficit.

The other big difference between Hungary and Argentina is the demographic one. Argentina was a comparatively high fertility developing economy, with, by and large, the phenomenon known as the demographic dividend out there in front of it. Hungary unfortunately belongs to that group of countries who went through a large part of their demographic transition before they became economically rich. As such the future lying out in front of Hungary is inevitably a complicated one, with or without the present economic conundrum. Fertility is at the lowest-low level (or see the file linked to here) and Hungary is set to age rapidly as the currently low life expectancy rises and rises. So the demographic changes which are facing Hungary involve more of a demographic penalty than a demographic dividend.

And Bokros is right to draw attention to the social spending dilemma which Hungary faces. He is also right that the pension and health systems badly need reform. The question is, as people enter a necessary private pillar, where does the money come from to finance the earlier PAYGO system, and how do you prevent the quality and availability of public services from eroding (which Bokros says he wants to do) if what you are going to do is reduce spending on them significantly? Somehow the numbers here just don't add up.

At the end of the day all comparisons are rather limited in their value. But what worries me most here is that I just can't see a sustainable path for Hungary to take hold of, and that, believe me, is the most worrying thing of all. Simply telling people that what they need is an austerity package if you have no clear idea of how the hell it can all work is only likely to mean that you end up as Cavallo did, only as I said Hungary isn't Argentina, and the end product of all this prevarication won't be a pretty sight.

Wednesday, November 22, 2006

Democracy In Hungary

The Economist Intelligence Unit has published the latest edition of its Democracy Index. As Portfolio Hungary reports, Hungary finds itself in 38th place, tucked in amongst the flawed democracies. It should not escape our notice that another of the EUs problem economies, Italy, is also well down the list in 34th position. The fact that both these societies are struggling with their government deficit and find it difficult to create a social consensus around the measures which need to be taken (and that both lean very heavily on tax increases in their adjustment programmes)seems somehow to be deeply significant.

Indeed I was only recently commenting on the rather favourable comparison which can be made about Spain's progress vis-a-vis Italy in this regard (Spain is in 16th place in the EIU list), and here we could mention that the rather more economically successful Czech Republic is notably in 18th place and well above the flawed democracy ranking. Someone somewhere should be thinking very hard about all this.

Indeed I was only recently commenting on the rather favourable comparison which can be made about Spain's progress vis-a-vis Italy in this regard (Spain is in 16th place in the EIU list), and here we could mention that the rather more economically successful Czech Republic is notably in 18th place and well above the flawed democracy ranking. Someone somewhere should be thinking very hard about all this.

No Euro Membership in Sight

This at least is the opinion of National Bank of Hungary governor Zsigmond Járai:

The government's present convergence program will not permit Hungary to adopt the euro, central-bank governor Zsigmond Járai said on Wednesday at a conference organized by the National Bank of Hungary on the country's past inflationary experiences.

The National Bank of Hungary previously expected Hungary to adopt the euro in 2007 or 2008, then extended the date to 2010; however it is no longer possible to tell when Hungary will be able to adopt the single European currency, Járai said. The central bank president asserted that the convergence program does not help improve the competitiveness of businesses in the country, increases tax burdens without broadening the tax base, while reducing the performance of the economy and economic growth. "Companies shouldn't calculate on the euro in their mid-term plans," Járai added.

Obviously Járai has some issues to battle out with the present government, and we shouldn't forget that only yesterday former Prime Minister Péter Medgyessy was having a go at the central bank, blaming them for their earlier monetary policy. Without entering directly into the politics of this, what Járai is saying makes a lot of sense. It is hard to see how job growth can be sustained with the present tax hike, and there is obviously going to be a reduction in domestic demand growth. But probably the most worrying issue is the present level of the Forint, coupled with the ongoing inflation, this will make exporting very hard work indeed, especially if the eurozone slows going into 2007. Clearly the central bank has a lot less responsibility for the mess than the politicians do, but the most worrying point of all is that there seems to be no direct sustainable path available for anyone to follow. I will fill in the details on this argument as we move forward. Bottom line, as the man says, don't count on Hungary joining the eurozone any time in the foreseeable future.

The government's present convergence program will not permit Hungary to adopt the euro, central-bank governor Zsigmond Járai said on Wednesday at a conference organized by the National Bank of Hungary on the country's past inflationary experiences.

The National Bank of Hungary previously expected Hungary to adopt the euro in 2007 or 2008, then extended the date to 2010; however it is no longer possible to tell when Hungary will be able to adopt the single European currency, Járai said. The central bank president asserted that the convergence program does not help improve the competitiveness of businesses in the country, increases tax burdens without broadening the tax base, while reducing the performance of the economy and economic growth. "Companies shouldn't calculate on the euro in their mid-term plans," Járai added.

Obviously Járai has some issues to battle out with the present government, and we shouldn't forget that only yesterday former Prime Minister Péter Medgyessy was having a go at the central bank, blaming them for their earlier monetary policy. Without entering directly into the politics of this, what Járai is saying makes a lot of sense. It is hard to see how job growth can be sustained with the present tax hike, and there is obviously going to be a reduction in domestic demand growth. But probably the most worrying issue is the present level of the Forint, coupled with the ongoing inflation, this will make exporting very hard work indeed, especially if the eurozone slows going into 2007. Clearly the central bank has a lot less responsibility for the mess than the politicians do, but the most worrying point of all is that there seems to be no direct sustainable path available for anyone to follow. I will fill in the details on this argument as we move forward. Bottom line, as the man says, don't count on Hungary joining the eurozone any time in the foreseeable future.

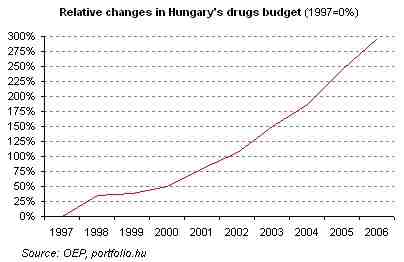

Paying For The Drugs

The above graphic (which comes from Portfolio Hungary) shows the relentless rise in the Hungarian drugs budget from 1997 to 2006. Now as explained in this post, Hungary is currently passing through what some have termed the second epidemiological transition. But this transition, unlike the first one, is not driven by improved nutrition in childhood and better public health, but rather life expectancy here is pushed up (from Hungary's comparatively low level of 68.45 - in the case of men) to levels which are more common elsewhere in the EU by the combined application of improved medicines and intensive medical care, both of which have significant costs associated with them. Hence the rise and rise of the drugs budget.

The big question, of course, is who will pay for this? Given the dire straits in which Hungarian public finance finds itself the answer seems far from clear, and this dilema is reflected in the current 'robbing Peter to pay Paul' tussle which the government and the major Hungarian drugs manufacturers are having.

The Hungarian Parliament has now passed what is supposed to be the final version of the new drug thrift bill. Portfolio Hungary offer a summary of just how the new regulation's impact on Hungary's listed pharmas Egis and Richter:

Key points of the Drug Economy Act:

- 12% flat rebate on all drug subsidies;

- annual HUF 5 million fee / sales representative;

- basis of producers' split payments into drugs budget is HUF 287 bn;

- joint coverage of spending overshoot by producers and state up to 9% miss (the larger the deficit, the higher drug makers' contribution is);

- full coverage of overshoot beyond 9% by producers;

- the section of the Act on the financing of the deficit was formulated highly ambiguously, but the Health Ministry confirmed that the objective of the regulation is that producers would contribute to the coverage of the deficit in ratio of the surplus of their subsidies relative to the subsidy they were granted in the previous year.

The latest development is positive for both Egis and Richter, given that the size of their subsidies will not be larger in 2007 than this year.

Just how these measures will affect the profitability and net worth of the two majors is, at this stage anyone's guess. But as Portfolio Hungary point out given the inbuilt tendency for the demand for medicines to grow it is hardly likely that the current measures will produce a net reduction in the budget:

At the same time we must keep in mind that drug subsidies have been growing dynamically for years. Annual average increase reached 17% since 1997 and has accelerated since 2001. Considering the rise in consumption in the past years we believe the government's measures would be enough only to halt growth.

Naturally the drugs majors are resisting the idea that this will be the final version of the bill going into law, and the latest news is that they have asked President László Sólyom not to sign the bill on the grounds that it is unconstitutional:

The association of Hungarian drug producers (MAGYOSZ) has asked President László Sólyom not to sign a bill on drug subsidies into law and ask for a review by the Constitutional Court, Richter has announced on Wednesday.

The association will argue that the bill, approved by Parliament on Monday, puts an unfair burden on domestic producers and generic firms and is therefore unconstitutional.

"We're still in the process of spelling out our argument but we will send him our letter today," Reuters cited spokeswoman Judit Tóth as saying.

President Sólyom will have five days from the time he received the bill to decide whether to sign the bill into law, send it back to Parliament for reconsideration or ask for a constitutional review from the Constitutional Court.

Which is all well and good, except that in the meantime someone somewhere has to decide just how the Hungarian deficit is actually going to be reduced.

Tuesday, November 21, 2006

Sustaining The Debt

Now I am not going to enter the political squabble which are going on all over the place, but I think former Prime Minister Péter Medgyessy draws attention to an important issue here: the rising cost of servicing the debt. Doubtless this was another factor in today's rate hold decision. Probably it is very unfair to blame the central bank for all these ills though, the current high rates are undoubtedly part of the general economic and financial crisis which Hungary is facing:

“The bank perfectly mistrusted the government,” wrote Medgyessy, premier from 2002 to 2004. “The unwarranted high level of interest rates grossly increased the government's expenses, chasing economic policy into a vicious cycle.” Medgyessy said the bank, which had cut its benchmark rate seven times in five months before he took office, for erasing half those cuts within three months of the vote. The former premier missed budget deficit targets every year in office and Hungary hasn't met its annual goals since. A telephone message left for spokesman Gábor Missura at the central bank seeking comment wasn't immediately returned. Public debt is set to rise to 72.3% of gross domestic product by 2008 from 62.3% last year, according to the government's projection. That's above the 60% limit for euro adoption. Medgyessy was forced out amid a coalition dispute and the lowest support for his Socialist Party in three years. He was replaced by Ferenc Gyurcsány, who led the coalition to a second consecutive term in the April election and stared measures to cut the budget shortfall, the European Union's widest. “It has been obviously proven by now that the switch of prime ministers was at the right time and was successful and fruitful for the coalition,” Medgyessy wrote. “The new government's reform momentum is unquestionable.” Gyurcsány raised taxes and cut subsidies to trim the shortfall and wants to overhaul the country's health care, education, pensions, local governments and public administration. That may be too much, according to Medgyessy. The government “is overreaching on reforms,” Medgyessy wrote. Overhauling that many sectors of the economy “isn't possible to carry out -- it results in frittering away energies and opens fronts against all social strata.” Medgyessy is now a traveling ambassador in Gyurcsány's government. He may be the premier's choice to replace central bank President Zsigmond Járai when his term expires next March, Web site Hirszerző said in April. (Bloomberg)

Meantime the comparatively high yields on Hungarian debt continue to drive the forint up:

Hungary's forint advanced to its highest in more than eight months as investors bought forint- denominated debt, the highest-yielding in the European Union.

The forint climbed for a second day as foreign holdings of Hungarian bonds surged to a record high of Ft 2.92 trillion ($14.5 billion) yesterday after the country's central bank kept its benchmark interest rate on hold at 8%. “The central bank's decision to leave rates unchanged triggered a rally for Hungarian bonds, which supported the forint,” said Martin Blum, head of emerging-market strategy at Bank Austria Creditanstalt AG.

The yield advantage offered by Hungarian debt securities is prompting foreign investors to buy forint-denominated bonds. The yield difference, or spread, investors demand to hold Hungarian 10-year debt rather than similar-maturity German bunds is 318 basis points, compared with 299 basis points six months ago.

Even as the yield on government bonds now starts to turn due to the high demand:

Hungary's Government Debt Management Agency (ÁKK) has received HUF 125.7 billion worth of bids on HUF 30 billion 3-month discount T-bills (D070228) at an auction on Tuesday. The 4.2x bid/cover ratio was not enough for the ÁKK to sell more of the instrument than originally planned.

The bills were sold at an average yield of 7.98%, down 17 basis points from Monday's benchmark fixing (of series D070314), but 6 bps up from the previous auction a week ago.

The ÁKK will offer HUF 45 bn and HUF 40 bn worth of 5-yr and 10-yr bonds, respectively at auctions on Thursday.

“The bank perfectly mistrusted the government,” wrote Medgyessy, premier from 2002 to 2004. “The unwarranted high level of interest rates grossly increased the government's expenses, chasing economic policy into a vicious cycle.” Medgyessy said the bank, which had cut its benchmark rate seven times in five months before he took office, for erasing half those cuts within three months of the vote. The former premier missed budget deficit targets every year in office and Hungary hasn't met its annual goals since. A telephone message left for spokesman Gábor Missura at the central bank seeking comment wasn't immediately returned. Public debt is set to rise to 72.3% of gross domestic product by 2008 from 62.3% last year, according to the government's projection. That's above the 60% limit for euro adoption. Medgyessy was forced out amid a coalition dispute and the lowest support for his Socialist Party in three years. He was replaced by Ferenc Gyurcsány, who led the coalition to a second consecutive term in the April election and stared measures to cut the budget shortfall, the European Union's widest. “It has been obviously proven by now that the switch of prime ministers was at the right time and was successful and fruitful for the coalition,” Medgyessy wrote. “The new government's reform momentum is unquestionable.” Gyurcsány raised taxes and cut subsidies to trim the shortfall and wants to overhaul the country's health care, education, pensions, local governments and public administration. That may be too much, according to Medgyessy. The government “is overreaching on reforms,” Medgyessy wrote. Overhauling that many sectors of the economy “isn't possible to carry out -- it results in frittering away energies and opens fronts against all social strata.” Medgyessy is now a traveling ambassador in Gyurcsány's government. He may be the premier's choice to replace central bank President Zsigmond Járai when his term expires next March, Web site Hirszerző said in April. (Bloomberg)

Meantime the comparatively high yields on Hungarian debt continue to drive the forint up:

Hungary's forint advanced to its highest in more than eight months as investors bought forint- denominated debt, the highest-yielding in the European Union.

The forint climbed for a second day as foreign holdings of Hungarian bonds surged to a record high of Ft 2.92 trillion ($14.5 billion) yesterday after the country's central bank kept its benchmark interest rate on hold at 8%. “The central bank's decision to leave rates unchanged triggered a rally for Hungarian bonds, which supported the forint,” said Martin Blum, head of emerging-market strategy at Bank Austria Creditanstalt AG.

The yield advantage offered by Hungarian debt securities is prompting foreign investors to buy forint-denominated bonds. The yield difference, or spread, investors demand to hold Hungarian 10-year debt rather than similar-maturity German bunds is 318 basis points, compared with 299 basis points six months ago.

Even as the yield on government bonds now starts to turn due to the high demand:

Hungary's Government Debt Management Agency (ÁKK) has received HUF 125.7 billion worth of bids on HUF 30 billion 3-month discount T-bills (D070228) at an auction on Tuesday. The 4.2x bid/cover ratio was not enough for the ÁKK to sell more of the instrument than originally planned.

The bills were sold at an average yield of 7.98%, down 17 basis points from Monday's benchmark fixing (of series D070314), but 6 bps up from the previous auction a week ago.

The ÁKK will offer HUF 45 bn and HUF 40 bn worth of 5-yr and 10-yr bonds, respectively at auctions on Thursday.

National Bank of Hungary Holds Rates At 8%

This decision is hardly surprising given the level of the forint and yesterdays construction numbers.

The National Bank of Hungary (NBH) has on Monday decided to leave the base rate unchanged at 8.00%.

As I say, apart from the forint this was presumeably not far from the front of their minds:

Construction sector output falls 3.3% yr/yr in August

Output volume of Hungary's construction sector fell 3.7% in September compared to the same month a year earlier, according to working-day adjusted and decreased 4.8% according to unadjusted figures, the Central Statistics Office (KSH) reported on Monday.

Compared to August, output was up a seasonally- and working day-adjusted 2.7%. In the first nine months of 2006, output volume of the construction sector fell 2.1% from the same period last year. At current prices, construction sector output was worth Ft 236.2 billion (€915.5 million) in September and it was worth Ft 1,426.7 billion in January-August.

The National Bank of Hungary (NBH) has on Monday decided to leave the base rate unchanged at 8.00%.

As I say, apart from the forint this was presumeably not far from the front of their minds:

Construction sector output falls 3.3% yr/yr in August

Output volume of Hungary's construction sector fell 3.7% in September compared to the same month a year earlier, according to working-day adjusted and decreased 4.8% according to unadjusted figures, the Central Statistics Office (KSH) reported on Monday.

Compared to August, output was up a seasonally- and working day-adjusted 2.7%. In the first nine months of 2006, output volume of the construction sector fell 2.1% from the same period last year. At current prices, construction sector output was worth Ft 236.2 billion (€915.5 million) in September and it was worth Ft 1,426.7 billion in January-August.

Friday, November 17, 2006

To Raise Or Not To Raise, That Is The Question

The debate currently taking place at the Hungarian central bank (the NBH) about the future course of interest rates is simply a reflection of the cleft stick that Hungarian monetary policy finds itself in at present. Raising rates will slow domestic growth and contain inflation, but it will also push up the Forint, and hence make it more difficult to export, and exports are what Hungary badly needs right now. No easy answers here:

According to the local media, National Bank of Hungary (NBH) Governor Zsigmond Járai said that a rate increase was not the only policy option on Monday, since the HUF rally would reduce inflationary pressures. Goldman Sachs has said on Friday the statement creates some downside risk to their forecast of a 25-basis-oint hike to 8.25% next Monday, since Járai is usually relatively hawkish in his comments. Goldman Sachs, however, sticks with its view.

At the last meeting, the MPC split three ways, with the doves supporting a pause and the hawks pushing for a 50-bp hike.

“We believe Monday's hike will be the final hike of the current cycle, but see some risk that the NBH will raise rates even further over concerns that inflation expectations are becoming entrenched," Rory MacFarquhar noted.

He expects inflation to peak at around 8% at the end of the first quarter next year.

But after that, he forecasts that “the contractionary effect of the deficit reduction programme will begin to outweigh the impact of higher tax rates and administered price increases."

According to the local media, National Bank of Hungary (NBH) Governor Zsigmond Járai said that a rate increase was not the only policy option on Monday, since the HUF rally would reduce inflationary pressures. Goldman Sachs has said on Friday the statement creates some downside risk to their forecast of a 25-basis-oint hike to 8.25% next Monday, since Járai is usually relatively hawkish in his comments. Goldman Sachs, however, sticks with its view.

At the last meeting, the MPC split three ways, with the doves supporting a pause and the hawks pushing for a 50-bp hike.

“We believe Monday's hike will be the final hike of the current cycle, but see some risk that the NBH will raise rates even further over concerns that inflation expectations are becoming entrenched," Rory MacFarquhar noted.

He expects inflation to peak at around 8% at the end of the first quarter next year.

But after that, he forecasts that “the contractionary effect of the deficit reduction programme will begin to outweigh the impact of higher tax rates and administered price increases."

Ferenc Puskás and Life Expectancy

Today we learn of the sad death of Ferenc Puskás at the age of 79. Puskás was undoubtedly a great footballer (you can find an interesting page about him on wikipedia) and he will be missed by family and football fans alike. Puskás reached the comparatively advanced age of 79, and we hope he enjoyed his later life. We may also like to note that Puskás lived considerably longer than the majority of Hungarian men, since the average male life expectancy is currently some 68.45 years. And it is here that the economic part of our story begins.

Life expectancy in Hungary continues to be comparatively young by European standards, so it is to be hoped that in the coming years this situation will improve considerably, but how exactly will this improvement affect the economic outlook for Hungary, that is also the question?

Now one thing is clear, any increase in life expectancy in Hungary will come by people who are now over 60 living longer. As this happens it will be wonderful news for everyone, but in economic terms this will have an important on cost, since it will involve a considerable expenditure in medical care and medicine, and it is just the question of who is going to pay for this which is the subject of considerable dispute between the Hungarian government and the pharmaceutical companies:

“We see if the modification would get approved it could lower the payment obligation of both Egis and Richter arising from tax on drug subsidies to HUF 1.5bn (when compared to the earlier version of 14%-16% tax resulting in HUF 2.0bn) and to HUF 2.4bn (when compared to the earlier version of 14%-16% tax resulting in HUF 3.3bn) for 2007 respectively," KBC's Barbara Jánosi said on Friday.

She added this step would be only a little positive development for these two companies when compared to substantial increase seen in their payment obligation from co-financing the gap of the drug subsidy budget.

According to the Parliament's latest decision, next year's drug subsidy budget target will be HUF 287 billion when compared to HUF 364 bn reported earlier by the Finance Ministry.

“We see the lowered target could lift substantially the budget gap for next year resulting in higher payment obligation for drug makers (if no changes will be in the distribution principles of the gap between industry participants)," Jánosi added.

Now it is clear that with this current comparatively low life expectancy some considerable improvement is to be hoped for and expected. If we take a look at a comparable society, the old east Germany, we can see that such an improvement can occur relatively quickly, if the right care and clinical environment is available.

Last year I had a post about this situation on a Fistful of Euros, based on a paper by the German-based researcher Marc Luy. Essentially the point is that after years of life expectancy divergence, the two societies - East and West - converged again comparatively rapidly in the 1990s based largely on what Luy calls the availability of nursing care:

“The demographic changes and developments in Eastern and Western Germany are generally seen to offer a unique possibility to understand the interaction between societal, social respective economic conditions and population processes. Almost identical demographic composition and behaviour until 1945 were followed by 45 years of life under different political and socio-economic structures resulting in completely different demographic conditions…. With Reunification in 1990 the population in Eastern Germany returned to the Western societal and economic system what caused sudden changes in all its demographic developments. These special preconditions lead some scholars to describe the Eastern German population as a kind of 'natural experiment' generated a large number of researches about changes in Eastern German demography.”

“In the field of mortality research especially the rapid convergence of survival conditions since 1990 following roughly two decades of continuous divergence are subject of central interest. The fact that both, the former increase and the recent decrease of the life expectancy gap between West and East Germany were mainly caused by age groups between 60 and 80 led to the central message that "it's never too late" for increasing length of life.”

So on the face of it a convergence of Hungarian life expectancy towards levels which are regarded as rather normal in the West European parts of the EU is to be expected, but we need to think about how this can be paid for.

Now many attribute Germany's current public finance problems to the incorporation of East Germany, and this view is *both* right and wrong.

It is wrong in the sense that it doesn't take account of the fact that ageing is an *all Germany* phenomenon, but it is right that the rapid increase in life expectancy that took place in East Germany in the 1990s simply piled on, and piled on the costs, and this must be a big part of the current financial crisis that the German health system is experiencing.

So all I am saying at this point is that the sum total of these effects will make the managing of the Hungarian deficit issue a bigger rather than a smaller headache, and the sooner the body politic in Hungary wakes up to this the better.

Life expectancy in Hungary continues to be comparatively young by European standards, so it is to be hoped that in the coming years this situation will improve considerably, but how exactly will this improvement affect the economic outlook for Hungary, that is also the question?

Now one thing is clear, any increase in life expectancy in Hungary will come by people who are now over 60 living longer. As this happens it will be wonderful news for everyone, but in economic terms this will have an important on cost, since it will involve a considerable expenditure in medical care and medicine, and it is just the question of who is going to pay for this which is the subject of considerable dispute between the Hungarian government and the pharmaceutical companies:

“We see if the modification would get approved it could lower the payment obligation of both Egis and Richter arising from tax on drug subsidies to HUF 1.5bn (when compared to the earlier version of 14%-16% tax resulting in HUF 2.0bn) and to HUF 2.4bn (when compared to the earlier version of 14%-16% tax resulting in HUF 3.3bn) for 2007 respectively," KBC's Barbara Jánosi said on Friday.

She added this step would be only a little positive development for these two companies when compared to substantial increase seen in their payment obligation from co-financing the gap of the drug subsidy budget.

According to the Parliament's latest decision, next year's drug subsidy budget target will be HUF 287 billion when compared to HUF 364 bn reported earlier by the Finance Ministry.

“We see the lowered target could lift substantially the budget gap for next year resulting in higher payment obligation for drug makers (if no changes will be in the distribution principles of the gap between industry participants)," Jánosi added.

Now it is clear that with this current comparatively low life expectancy some considerable improvement is to be hoped for and expected. If we take a look at a comparable society, the old east Germany, we can see that such an improvement can occur relatively quickly, if the right care and clinical environment is available.

Last year I had a post about this situation on a Fistful of Euros, based on a paper by the German-based researcher Marc Luy. Essentially the point is that after years of life expectancy divergence, the two societies - East and West - converged again comparatively rapidly in the 1990s based largely on what Luy calls the availability of nursing care:

“The demographic changes and developments in Eastern and Western Germany are generally seen to offer a unique possibility to understand the interaction between societal, social respective economic conditions and population processes. Almost identical demographic composition and behaviour until 1945 were followed by 45 years of life under different political and socio-economic structures resulting in completely different demographic conditions…. With Reunification in 1990 the population in Eastern Germany returned to the Western societal and economic system what caused sudden changes in all its demographic developments. These special preconditions lead some scholars to describe the Eastern German population as a kind of 'natural experiment' generated a large number of researches about changes in Eastern German demography.”

“In the field of mortality research especially the rapid convergence of survival conditions since 1990 following roughly two decades of continuous divergence are subject of central interest. The fact that both, the former increase and the recent decrease of the life expectancy gap between West and East Germany were mainly caused by age groups between 60 and 80 led to the central message that "it's never too late" for increasing length of life.”

So on the face of it a convergence of Hungarian life expectancy towards levels which are regarded as rather normal in the West European parts of the EU is to be expected, but we need to think about how this can be paid for.

Now many attribute Germany's current public finance problems to the incorporation of East Germany, and this view is *both* right and wrong.

It is wrong in the sense that it doesn't take account of the fact that ageing is an *all Germany* phenomenon, but it is right that the rapid increase in life expectancy that took place in East Germany in the 1990s simply piled on, and piled on the costs, and this must be a big part of the current financial crisis that the German health system is experiencing.

So all I am saying at this point is that the sum total of these effects will make the managing of the Hungarian deficit issue a bigger rather than a smaller headache, and the sooner the body politic in Hungary wakes up to this the better.

Fitch On Hold

The credit rating agency Fitch are adopting a wait and see attitude towards Gyurcsány's reform package before taking any decision on an adjustment in the sovereign rating:

Hungary's credit rating depends on Prime Minister Ferenc Gyurcsány's ability to push his fiscal reform package, Fitch ratings agency's sovereign ratings analyst Edward Parker said on Friday.

"We think they will make some good progress but the Prime Minister's lie dented his personal authority and obviously implementing the policies are unpopular," Reuters cited Parker as telling reporters at a Fitch conference on emerging markets.

Fitch has assigned Hungary a sovereign rating of BBB+ with a negative outlook.

"The rating depends on if the prime minister can reduce the deficit and stabilise the economy. We think the government can make progress on reducing the deficit. Our central scenario remains that they reduce it from 10% (of GDP) to around 4.5% to 5% by 2008," Parker said.

Hungary's credit rating depends on Prime Minister Ferenc Gyurcsány's ability to push his fiscal reform package, Fitch ratings agency's sovereign ratings analyst Edward Parker said on Friday.

"We think they will make some good progress but the Prime Minister's lie dented his personal authority and obviously implementing the policies are unpopular," Reuters cited Parker as telling reporters at a Fitch conference on emerging markets.

Fitch has assigned Hungary a sovereign rating of BBB+ with a negative outlook.

"The rating depends on if the prime minister can reduce the deficit and stabilise the economy. We think the government can make progress on reducing the deficit. Our central scenario remains that they reduce it from 10% (of GDP) to around 4.5% to 5% by 2008," Parker said.

Thursday, November 16, 2006

Wages, Budget Deficits Etc

The principal news today is that real wage growth slowed year-on-year in the period between January and September 2006. This is hardly surprising, but equally it would be even more surprising if real wage growth in the coming six months didn't slow considerably more.

Hungary's September gross wages slowed significantly to 7.1% year on year from 10.8% yr/yr. The deceleration was more meaningful in the private sector (down to 7.6% yr/yr from 11.7% yr/yr). Public sector wage growth also moderated to 6.9% yr/yr from 9.3% yr/yr.

If we take into account inflation, then obviously real wage growth is considerably less:

Real wages in Hungary rose 4.8% yr/yr in January-September 2006, based on an 8.0% increase in net monthly wages from the same period of 2005 and an average CPI of 3.1%, the Central Statistics Office (KSH) announced on Thursday.

In fact if we look at what has been happening more recently we will find that real wages are now actually falling:

In September alone, real wages dropped 1.8% year on year, Econews calculated, based on a 4.0% year on year rise in net wages and twelve-month CPI of 5.9% in September.

As István Zsoldos from Goldman Sachs observes:

“These figures are still relatively high, although lower than the August ones that were boosted by bonus payments ahead of wage tax increases."

“We think that the NBH will remain worried about inflation expectations becoming entrenched and will hike rates by another 25 bps next Monday. Currently we are forecasting that this is going to be the top of the hiking cycle, but there is still a significant risk that the NBH might go further."

“Inflation will only peak in March next year, at around 8%, and worries about inflation expectations picking up will not go away at least until then, in our view."

Which all means than many think (and I concur) that the National Bank of Hungary is more than likely going to raise rates on 20th November:

The Hungarian statistics office's Tuesday report about a pick-up in inflation in October (6.3% vs. 5.9% in Sept ) and the forint's gradual strengthening against the euro have not changed the consensus estimate in merit that Portfolio.hu's poll showed on Monday. In that survey analysts have projected that the Monetary Council will raise the base rate by 25 basis points to 8.25% on 20 November. At the same time it is a crucial change in views from a month ago that now the respondents believe the end of the central bank's (NBH) rate hike streak will be reached this month.

Meantime the finance ministry is highlighting the fact that they will post (unexpectedly) a deficit in December:

In a rather unusual move, Hungary's Finance Ministry has on Thursday projected HUF 24.9 billion public sector deficit for December 2006 (cash based, excluding local governments), while in the last month of the year, the budget generally posts a surplus over booming tax and contribution revenues. Due to a technical reason, it will be different this year.

A little embarrassing this 'technical' detail, especially since Moody's have just made it known that some of their officials are currently on a visit to Hungary, of course there is nothing to worry about, since this is simply a 'regular' visit (hmm, hmm):

Officials of ratings agency Moody's are on a visit in Hungary, Finance Ministry spokesman Ferenc Pichler told on Thursday, adding that this is but one of the regular meetings between ratings firms and the government.

"This is nothing extraordinary. Delegations from credit rating agencies come regularly," Pichler said, adding that officials from another rating agency were in Hungary on Wednesday. On 25 September, Moody's Investors Service placed Hungary's A1 local and foreign currency government bond ratings and its A1 foreign currency bank deposit ceiling rating on review for possible downgrade. This is three notches better than the rating of Standard & Poor's and Fitch. The agency has not changed the rating since 2002, but moved to negative outlook in February. István Zsoldos of Goldman Sachs said than that Moody's statement made it "very likely " that there would be a downgrade, adding that the question was whether it would be a one- or two-notch move. Pichler declined to comment a question whether there was a connection between the negative outlook and the visit of Moody's officials. (portfolio.hu)

Hungary's September gross wages slowed significantly to 7.1% year on year from 10.8% yr/yr. The deceleration was more meaningful in the private sector (down to 7.6% yr/yr from 11.7% yr/yr). Public sector wage growth also moderated to 6.9% yr/yr from 9.3% yr/yr.

If we take into account inflation, then obviously real wage growth is considerably less:

Real wages in Hungary rose 4.8% yr/yr in January-September 2006, based on an 8.0% increase in net monthly wages from the same period of 2005 and an average CPI of 3.1%, the Central Statistics Office (KSH) announced on Thursday.

In fact if we look at what has been happening more recently we will find that real wages are now actually falling:

In September alone, real wages dropped 1.8% year on year, Econews calculated, based on a 4.0% year on year rise in net wages and twelve-month CPI of 5.9% in September.

As István Zsoldos from Goldman Sachs observes:

“These figures are still relatively high, although lower than the August ones that were boosted by bonus payments ahead of wage tax increases."

“We think that the NBH will remain worried about inflation expectations becoming entrenched and will hike rates by another 25 bps next Monday. Currently we are forecasting that this is going to be the top of the hiking cycle, but there is still a significant risk that the NBH might go further."

“Inflation will only peak in March next year, at around 8%, and worries about inflation expectations picking up will not go away at least until then, in our view."

Which all means than many think (and I concur) that the National Bank of Hungary is more than likely going to raise rates on 20th November:

The Hungarian statistics office's Tuesday report about a pick-up in inflation in October (6.3% vs. 5.9% in Sept ) and the forint's gradual strengthening against the euro have not changed the consensus estimate in merit that Portfolio.hu's poll showed on Monday. In that survey analysts have projected that the Monetary Council will raise the base rate by 25 basis points to 8.25% on 20 November. At the same time it is a crucial change in views from a month ago that now the respondents believe the end of the central bank's (NBH) rate hike streak will be reached this month.

Meantime the finance ministry is highlighting the fact that they will post (unexpectedly) a deficit in December:

In a rather unusual move, Hungary's Finance Ministry has on Thursday projected HUF 24.9 billion public sector deficit for December 2006 (cash based, excluding local governments), while in the last month of the year, the budget generally posts a surplus over booming tax and contribution revenues. Due to a technical reason, it will be different this year.

A little embarrassing this 'technical' detail, especially since Moody's have just made it known that some of their officials are currently on a visit to Hungary, of course there is nothing to worry about, since this is simply a 'regular' visit (hmm, hmm):

Officials of ratings agency Moody's are on a visit in Hungary, Finance Ministry spokesman Ferenc Pichler told on Thursday, adding that this is but one of the regular meetings between ratings firms and the government.

"This is nothing extraordinary. Delegations from credit rating agencies come regularly," Pichler said, adding that officials from another rating agency were in Hungary on Wednesday. On 25 September, Moody's Investors Service placed Hungary's A1 local and foreign currency government bond ratings and its A1 foreign currency bank deposit ceiling rating on review for possible downgrade. This is three notches better than the rating of Standard & Poor's and Fitch. The agency has not changed the rating since 2002, but moved to negative outlook in February. István Zsoldos of Goldman Sachs said than that Moody's statement made it "very likely " that there would be a downgrade, adding that the question was whether it would be a one- or two-notch move. Pichler declined to comment a question whether there was a connection between the negative outlook and the visit of Moody's officials. (portfolio.hu)

Wednesday, November 15, 2006

From The Analysts

Portfolio Hungary published some of the analyst comments on the third quarter GDP data. István Zsoldos from Goldman Sachs seems pretty much to the point:

“The impact of the fiscal restrictions (which started in September) is still fairly limited in the Q3 figures."

“Wage growth was very strong before the September wage tax increases, and in our view that was the reason why consumption is probably still holding up (there is no detailed breakdown published at this release)."

“Private sector investment was surprisingly weak in Q2, and this component might have shown a rebound in Q3 as well."

“Overall, the Q3 data is going to be less important than the later quarters because the most significant question is how households are going to react to the full impact of the fiscal tightening. We expect to see signs of a serious slowdown in the Q4 data."

So the impact of the tightening is yet to make itself felt. Raffaella Tenconi from Dresdner Kleinwort seems excessively optimistic:

“Given the prospects for continuing buoyant eurozone growth, which will support exports, and rapid wage growth, supportive of consumer demand, growth is likely to decelerate only gradually in the near term."

The outlook for eurozone growth is much more uncertain, in particular see this from Claus Vistesen.

“The impact of the fiscal restrictions (which started in September) is still fairly limited in the Q3 figures."

“Wage growth was very strong before the September wage tax increases, and in our view that was the reason why consumption is probably still holding up (there is no detailed breakdown published at this release)."

“Private sector investment was surprisingly weak in Q2, and this component might have shown a rebound in Q3 as well."

“Overall, the Q3 data is going to be less important than the later quarters because the most significant question is how households are going to react to the full impact of the fiscal tightening. We expect to see signs of a serious slowdown in the Q4 data."

So the impact of the tightening is yet to make itself felt. Raffaella Tenconi from Dresdner Kleinwort seems excessively optimistic:

“Given the prospects for continuing buoyant eurozone growth, which will support exports, and rapid wage growth, supportive of consumer demand, growth is likely to decelerate only gradually in the near term."

The outlook for eurozone growth is much more uncertain, in particular see this from Claus Vistesen.

Healthcare in Hungary

One of the big topics I have yet to get into relating to the Hungarian situation is the demography. This will come a bit at a time as I ease myself in. But two factors evidently stand out here, the health care and the pensions system.

On the health front one of the factors which indicates the importance of demographic processes in the Hungarian situation is the relative importance of the big pharmaceutical companies (Richter Gedeon, Egis etc) in the economy and in payments to these companies in the general government finances picture. Many have spoken about the 'demographics' (as opposed to the demography) of ageing in terms of the 'product mix' that will be a feature of the consumption process, and here pharmaceutical products loom large (and this despite the fact that life expectancy in Hungary at 72.66 is still comparatively young by European standards, a detail which means that there is plenty of scope - as we have seen in East Germany - for extending life expectancy by intensifying medical care, but this of course, again as we are seeing in Germany, is expensive, very expensive). What many fail to note about the situation is the structural aspect, ie that there is s shift in consumption away from those who are able to pay towards those who need others to pay (either the state or children). This will have important macro economic consequences.

Some measure of the situation can be found in this Portfolio Hungary article from the end of October:

Hungary's drug subsidy budget will be 364 billion forints in 2007, below the expected 2006 spending of HUF 380 billion, Finance Ministry spokesman Ferenc Pichler told Portfolio.hu on Monday, confirming earlier press reports.

The HUF 364 bn figure is well above the HUF 320 bn most analysts and drug sector experts had expected for next year, and is obviously positive for producers. However, it is yet to be seen on Tuesday what gross budget, which excludes producers' contributions, the ministry expects for 2007. This information is to be of huge importance for pharmaceutical companies.

The higher-than-expected figure, or a lower-than-expected gap of the drug subsidy budget, is likely to reduce the expected contribution of the biggest listed producers, Richter and Egis, to the subsidy budget.

According to earlier press reports, the drugs budget was to be HUF 320 billion and the effective subsidy would have been HUF 440 bn in 2007. In this case, the contribution of producers would have been substantial, given that the National Health Insurance Fund (OEP) and the producers will jointly pay for an overshoot of the budget up to 9%, while any excess budget overspending above 9% will be solely covered by drug makers.

A budget of HUF 364 bn means that producers will not have to cover the overshoot fully up to HUF 467 bn worth of subsidies. As this year's effective subsidies are to reach HUF 380-400 bn, an overshoot larger than 9% is highly unlikely for 2007. (In other words, we do not believe next year's gross deficit will be over HUF 467 bn.)

Now at this point I am still really informing myself, and am not yet clear what the final details of the health budget for 2007 actually are (we won't know this till the final vote on Nov 20 it seems), but one thing is for sure, the cost of these subsidies is an important part of the public finance picture, and that reducing the subsidies significantly will hit the pharma sector hard, and by a knock-on effect the economy generally.

There is more news on this today:

Yet another amendment was made to Hungary's healthcare bill that may force pharmaceuticals to pay more into the drug budget in 2007 than planned in an earlier legislation, according to a Tuesday report by news agency Bloomberg.

Portfolio Hungary comments:

Unfortunately we find it impossible to determine which of the above proposals the committee wants to submit to Parliament. However, we would not be surprised if further modifications were made until the final vote on 20 November. Based on the current proposal, producers would have an easy job cutting their clawback - they would simply need to reduce the number of pills in boxes.

At the moment, it is also impossible to quantify the impact on the profits of either Egis or Richter.

The current uncertainties will not simply evaporate even after the bill is passed, since the size of clawback will depend on actual consumption, which cannot be assessed accurately as it hinges on different future measures that impact demand.

So the situation is a very uncertain one, but do not miss this point:

However, we would not be surprised if the act in the end would not contain a clawback obligation based on subsidy brackets. In this case, drug producers would simply need to lower the content of boxes to curb their payments into the National Health Insurance Fund (OEP).

So you can sell less for the same price. This seems to be yet another round of the 'stumbling and mumbling' which seems to have characterized the main approach to this crisis to date. Of course there must be many cases of 'inefficiency' in drug provision, with people getting more medicine than they need, but there must also be many cases of people actually needing the medicines they are prescribed, and in these cases if each box contains less then they will simply need to have more boxes, and especially in the critical non-generic sector, which is why, I suppose, there is so much uncertainty about the final costs and savings involved in the exercise. The whole approach smacks more of 'robbing Peter to pay Paul' than of anything else. And, I repeat, all of this seems set to have important and ongoing macroeconomic consequences.

On the health front one of the factors which indicates the importance of demographic processes in the Hungarian situation is the relative importance of the big pharmaceutical companies (Richter Gedeon, Egis etc) in the economy and in payments to these companies in the general government finances picture. Many have spoken about the 'demographics' (as opposed to the demography) of ageing in terms of the 'product mix' that will be a feature of the consumption process, and here pharmaceutical products loom large (and this despite the fact that life expectancy in Hungary at 72.66 is still comparatively young by European standards, a detail which means that there is plenty of scope - as we have seen in East Germany - for extending life expectancy by intensifying medical care, but this of course, again as we are seeing in Germany, is expensive, very expensive). What many fail to note about the situation is the structural aspect, ie that there is s shift in consumption away from those who are able to pay towards those who need others to pay (either the state or children). This will have important macro economic consequences.

Some measure of the situation can be found in this Portfolio Hungary article from the end of October:

Hungary's drug subsidy budget will be 364 billion forints in 2007, below the expected 2006 spending of HUF 380 billion, Finance Ministry spokesman Ferenc Pichler told Portfolio.hu on Monday, confirming earlier press reports.

The HUF 364 bn figure is well above the HUF 320 bn most analysts and drug sector experts had expected for next year, and is obviously positive for producers. However, it is yet to be seen on Tuesday what gross budget, which excludes producers' contributions, the ministry expects for 2007. This information is to be of huge importance for pharmaceutical companies.

The higher-than-expected figure, or a lower-than-expected gap of the drug subsidy budget, is likely to reduce the expected contribution of the biggest listed producers, Richter and Egis, to the subsidy budget.

According to earlier press reports, the drugs budget was to be HUF 320 billion and the effective subsidy would have been HUF 440 bn in 2007. In this case, the contribution of producers would have been substantial, given that the National Health Insurance Fund (OEP) and the producers will jointly pay for an overshoot of the budget up to 9%, while any excess budget overspending above 9% will be solely covered by drug makers.

A budget of HUF 364 bn means that producers will not have to cover the overshoot fully up to HUF 467 bn worth of subsidies. As this year's effective subsidies are to reach HUF 380-400 bn, an overshoot larger than 9% is highly unlikely for 2007. (In other words, we do not believe next year's gross deficit will be over HUF 467 bn.)

Now at this point I am still really informing myself, and am not yet clear what the final details of the health budget for 2007 actually are (we won't know this till the final vote on Nov 20 it seems), but one thing is for sure, the cost of these subsidies is an important part of the public finance picture, and that reducing the subsidies significantly will hit the pharma sector hard, and by a knock-on effect the economy generally.

There is more news on this today:

Yet another amendment was made to Hungary's healthcare bill that may force pharmaceuticals to pay more into the drug budget in 2007 than planned in an earlier legislation, according to a Tuesday report by news agency Bloomberg.

Portfolio Hungary comments:

Unfortunately we find it impossible to determine which of the above proposals the committee wants to submit to Parliament. However, we would not be surprised if further modifications were made until the final vote on 20 November. Based on the current proposal, producers would have an easy job cutting their clawback - they would simply need to reduce the number of pills in boxes.

At the moment, it is also impossible to quantify the impact on the profits of either Egis or Richter.

The current uncertainties will not simply evaporate even after the bill is passed, since the size of clawback will depend on actual consumption, which cannot be assessed accurately as it hinges on different future measures that impact demand.

So the situation is a very uncertain one, but do not miss this point:

However, we would not be surprised if the act in the end would not contain a clawback obligation based on subsidy brackets. In this case, drug producers would simply need to lower the content of boxes to curb their payments into the National Health Insurance Fund (OEP).

So you can sell less for the same price. This seems to be yet another round of the 'stumbling and mumbling' which seems to have characterized the main approach to this crisis to date. Of course there must be many cases of 'inefficiency' in drug provision, with people getting more medicine than they need, but there must also be many cases of people actually needing the medicines they are prescribed, and in these cases if each box contains less then they will simply need to have more boxes, and especially in the critical non-generic sector, which is why, I suppose, there is so much uncertainty about the final costs and savings involved in the exercise. The whole approach smacks more of 'robbing Peter to pay Paul' than of anything else. And, I repeat, all of this seems set to have important and ongoing macroeconomic consequences.

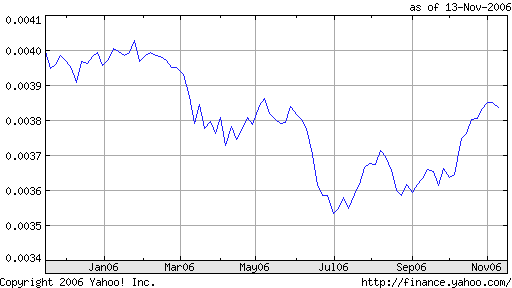

Hungarian Forint

The forint reacted positively to yesterday's GDP and inflation news. Since the news wasn't exactly unequivocally good I can only read this as suggesting that it wasn't as bad as it might have been, but these are early days still. Obviously one way to read this reaction is that people imagine the central bank will still raise interest rates, and that the relatively poor eurozone performance might mean that the ECB will not raise very much, but this is still far from clear (Claus Vistesen has some interesting comments on this situation). Obviously in the short term any increase in the interest rate differential would be forint positive, but this would not necessarily be good news for GDP growth inside Hungary, since given the expected weakening in internal consumer demand and the programme of government cuts Hungary badly needs to export, and with the forint at these levels (and possibly the eurozone slowing into 2007) this isn't necessarily going to be at all easy.

I have included a one year yahoo finance chart on the movement of the forint in this post, and it is clear that the forint has recovered most of the ground lost in the summer, so there will not be so much competitive advantage to be extracted, which makes, quite frankly, the current high inflation levels rather worrying. Bottom line: you need to think about the complete macro picture to see what is happening here.

Following October inflation figures and Q3 GDP data published this morning, the Hungarian forint broke out of its 258.50-262.00 range it has been confined to this month. The HUF firmed to 258 against the euro, a level not touched since mid-March. In late afternoon trade the forint was seen stabilising at 258.00/50 to the EUR.

The October inflation data (+6.2% yr/yr vs. 5.9% in Sept) prompted market participants to put off their expectations for the end of the rate hike streak a little bit further in time. The figure hints that the Monetary Council will decide on yet another 25-bp hike to 8.25% at its 20 November policy meeting.

Tuesday, November 14, 2006

October Inflation Numbers

Well inflation in October was just a touch higher than expected:

Hungary's consumer prices climbed 6.3% year on year in October, up from a 5.9% increase in September and overshooting analysts' consensus estimate of 6.2% in a Portfolio.hu poll conducted on Monday.

Even though this number was only very slightly above forecast it is hardly good news, since it will put pressure on the central bank to raise rates. The only saving grace in all this is that the ECB may come under increasing pressure not to raise rates further as economic growth and investor confidence in Germany deteriorate and this possibility, if confirmed, will put sort of floor under the Forint. However such a move would have to come over the protesting bodies of Trichet and many others at the ECB who keep insisting that inflation is still the primary threat. As I keep saying on my own blog, someone somewhere is going to have a hell of a lot of humble pie to eat at some point.

But even this possibity is very much a double edged sword, since slowing growth across the eurozone won't help Hungary to raise exports, which is something she badly needs to do. This is the meaning of being between a rock and a hard place.

Hungary's consumer prices climbed 6.3% year on year in October, up from a 5.9% increase in September and overshooting analysts' consensus estimate of 6.2% in a Portfolio.hu poll conducted on Monday.

Even though this number was only very slightly above forecast it is hardly good news, since it will put pressure on the central bank to raise rates. The only saving grace in all this is that the ECB may come under increasing pressure not to raise rates further as economic growth and investor confidence in Germany deteriorate and this possibility, if confirmed, will put sort of floor under the Forint. However such a move would have to come over the protesting bodies of Trichet and many others at the ECB who keep insisting that inflation is still the primary threat. As I keep saying on my own blog, someone somewhere is going to have a hell of a lot of humble pie to eat at some point.

But even this possibity is very much a double edged sword, since slowing growth across the eurozone won't help Hungary to raise exports, which is something she badly needs to do. This is the meaning of being between a rock and a hard place.

Hungarian Third Quarter Growth

Well year-on-year growth is slowing slightly, but hardly exceptionally so. This is neither surprising nor exceptional, but it is the first piece of hard data. The important question is still what happens next, as interest rates and the government 'correction' programme start to bite.

Hungary's gross domestic product grew by 3.6% year on year in the third quarter of 2006, according to first estimate figures released by the Central Statistics Office (KSH) on Tuesday. In Q2 the country's economy grew by 3.8% in annual terms.

The Budapest Business Journal have some useful background data: